If you’re still a while off retirement, superannuation is probably out of sight, out of mind. Your super may be growing in the background without much thought. However, small changes now may mean that you are setting yourself up for success when the time comes to start thinking seriously about your retirement plans.

So how can you get ahead by boosting your super now?

Check how your super is tracking

When was the last time you checked your super balance? If it has been a while, we encourage you to log in to your superannuation account to see how you are progressing and try to do this regularly.

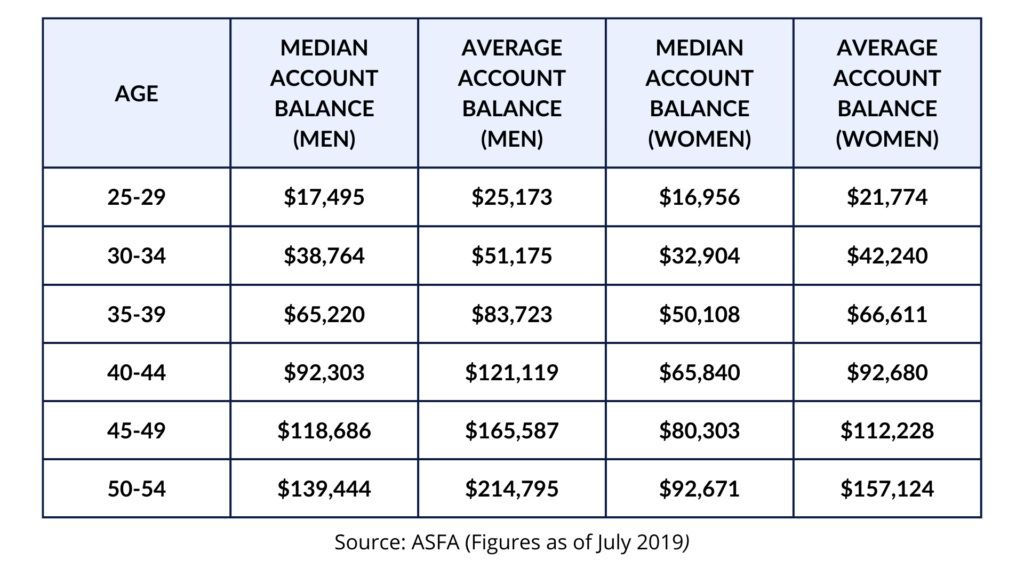

You can refer to the below table as a guide to how you are tracking with your super. Please note that this is just an average for your age and gender and may not meet your individual needs.

Superannuation balances by age and gender:

You can also use the handy Super Guru calculator to help you get an understanding of your progress!

Review your retirement goals

Now that you have checked in on how your super is tracking, it’s time to review your retirement goals and how much you need to save to comfortably meet your goals. Keep in mind that inflation will impact how much you need in the future!

3 tips to boost your super!

1. Review your Investments

According to research, about 80% of member superannuation funds are invested in the default option in a super fund chosen by their employer or award. But is this the best investment option for you and your plans for the future? Given these funds are designed to provide you with your ideal retirement, taking an active involvement in the investment of these funds is always wise. Speak to your Financial Planner about your best investment options.

2. Salary Sacrifice / Personal Deductible Contributions

You always have the option to pay more than the mandatory 10% from your employer. A little extra every week can make a big difference over an extended period.

You can set up a salary sacrifice arrangement with your employer whereby part of your pre-tax income is paid straight to your super. Salary sacrifice may also reduce your taxable income, which means you will pay less tax each pay period. Alternatively, you may be able to make a tax-deductible contribution to your superannuation. Your tax return will benefit from the tax deduction whilst you benefit from growing your retirement benefit.

3. Review your insurance

We recommend that you review your insurance regularly throughout your working life. Depending on your circumstances, you could benefit from taking out insurance within your fund. You could also opt out of these insurance options if you have this covered elsewhere, meaning that more will be contributing towards growing your super.

APS Financial Planning

If you’re ready to get serious about boosting your super, chat with the team at APS Financial Planning about the best options for your unique circumstances and goals.