Written by APS Financial Planner, Timothy Foster

Life today is busy! Whether you are focused on your career, buying your first home, making travel plans, getting married or starting a family, your thirties is often a period of many changes. With so much going on and so many years of work ahead of you, many do not think about their super.

Even if retirement is a long way off, you still have time on your side to build your retirement nestegg. Your thirties is the perfect time to create a retirement roadmap and set your future self up for success!

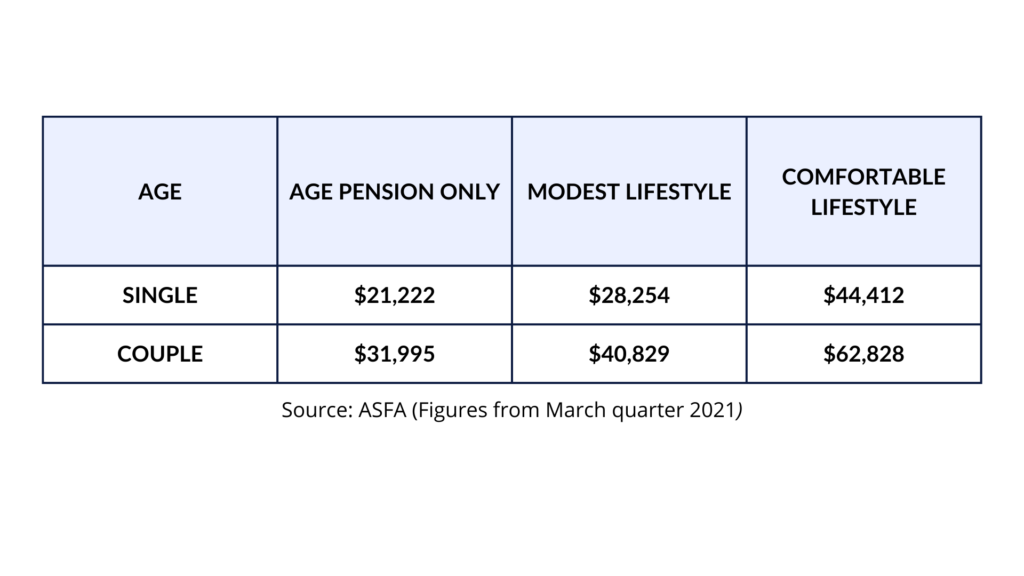

How much do you need to save for retirement?

According to the Australian Superannuation Funds of Australia (ASFA), the amount you need for retirement depends on what type of lifestyle you’re aiming for and whether you’re saving as a single or in a couple. Whilst your needs may vary, the setting and review of a target is the first step to successful planning.

Annual budget need to fund lifestyle in post-work years

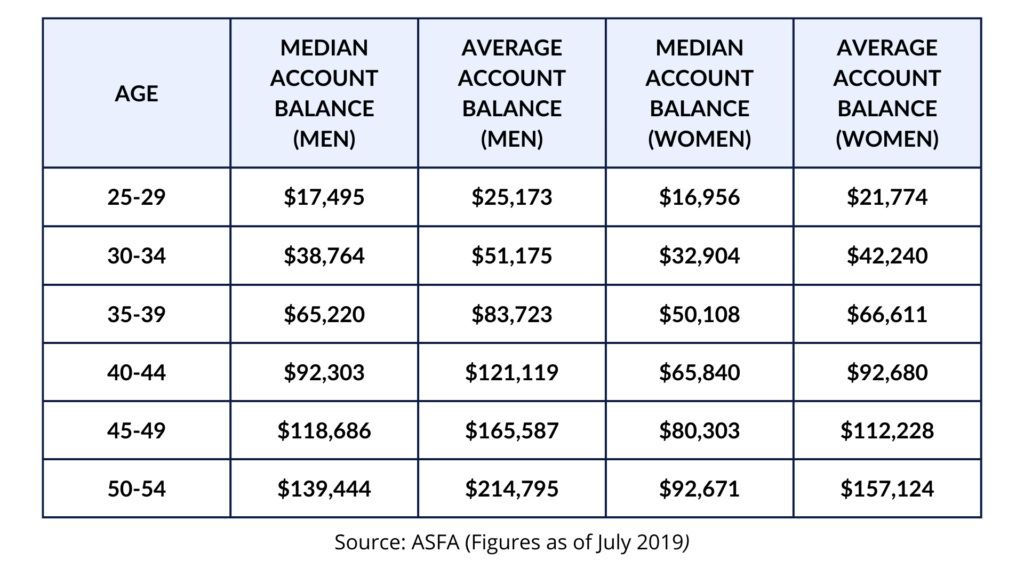

How are you tracking with your super?

When was the last time you checked your super balance? If it has been a while, we encourage you to log in to your superannuation account to see how you are progressing and try to do this regularly.

You can refer to the below table as a guide to how you are tracking with your super. Please note that this is just an average for your age and gender and may not meet your individual needs.

Superannuation balances by age and gender

You can also use the handy Super Guru calculator to help you get an understanding of your progress!

Strategies to give yourself a super boost

If you are concerned about your superannuation balance or if you are simply keen to get ahead while time is on your side, I have three useful tips to share.

1. Review your Investments

According to research, about 80% of members superannuation funds are invested in the default option in a super fund chosen by their employer or award. Of that 80%, it’s estimated that only 20% was chosen by the staff member with the remainder being a default option (see Part One of the final report at www.SuperSystemReview.gov.au for references). Is this the best investment option for you and your plans for the future? Does the risk level of this option meet your needs? Given these funds are designed to provide you with your ideal retirement, then taking an active involvement in the investment of these funds are wise.

2. Salary Sacrifice / Personal Deductible Contributions

You always have the option to pay more than the mandatory 10% from your employer. A little extra every week can make a big difference over an extended period.

You can set up a salary sacrifice arrangement with your employer whereby part of your pre-tax income is paid straight to your super. Salary sacrifice may also reduce your taxable income, which means you will pay less tax each pay period. Alternatively, you may be able to make a tax-deductible contribution to your superannuation. Your tax return will benefit from the tax deduction whilst you benefit from growing your retirement benefit.

3. Review your insurance

We recommend that you review your insurance regularly throughout your working life. Depending on your circumstances, you could benefit from taking out insurance within your fund. You could also opt-out for these insurance options if you have this covered elsewhere, meaning that more will be contributing towards growing your super.

Seek financial advice

Retirement planning and super may be at the bottom of your priority list right now, but there has never been a better time to seek advice and get ahead. If you leave it too late, you could be chasing your tail in your later years.

When you have a clear vision and a plan in place, you’ll be able to make your money work for you now and in the future.

Learn more about APS Financial Planning.

Written by APS Financial Planner, Timothy Foster

Timothy joined the APS Benefits Group in 2006 and launched the APS Financial Planning department. He is an experienced and respected financial planner who is committed to focusing on client needs and assisting them to maximise their financial assets. Timothy is well known for his simple and straightforward strategies designed to benefit his client’s future.

Timothy Foster’s qualifications include Certified Financial Planning (CFP), Life Risk Specialist (LRS) & Advanced Diploma of Financial Services (Financial Planning), with over 25 years experience in Financial Planning, Banking and Accounting, both within Australia and overseas. He has extensive experience in Government Superannuation funds, putting him in demand to speak at seminars and departments.

Outside of being a passionate Financial Planner, Timothy is a proud dad of two young children and loves travelling, be it outback Australia or just around the corner!